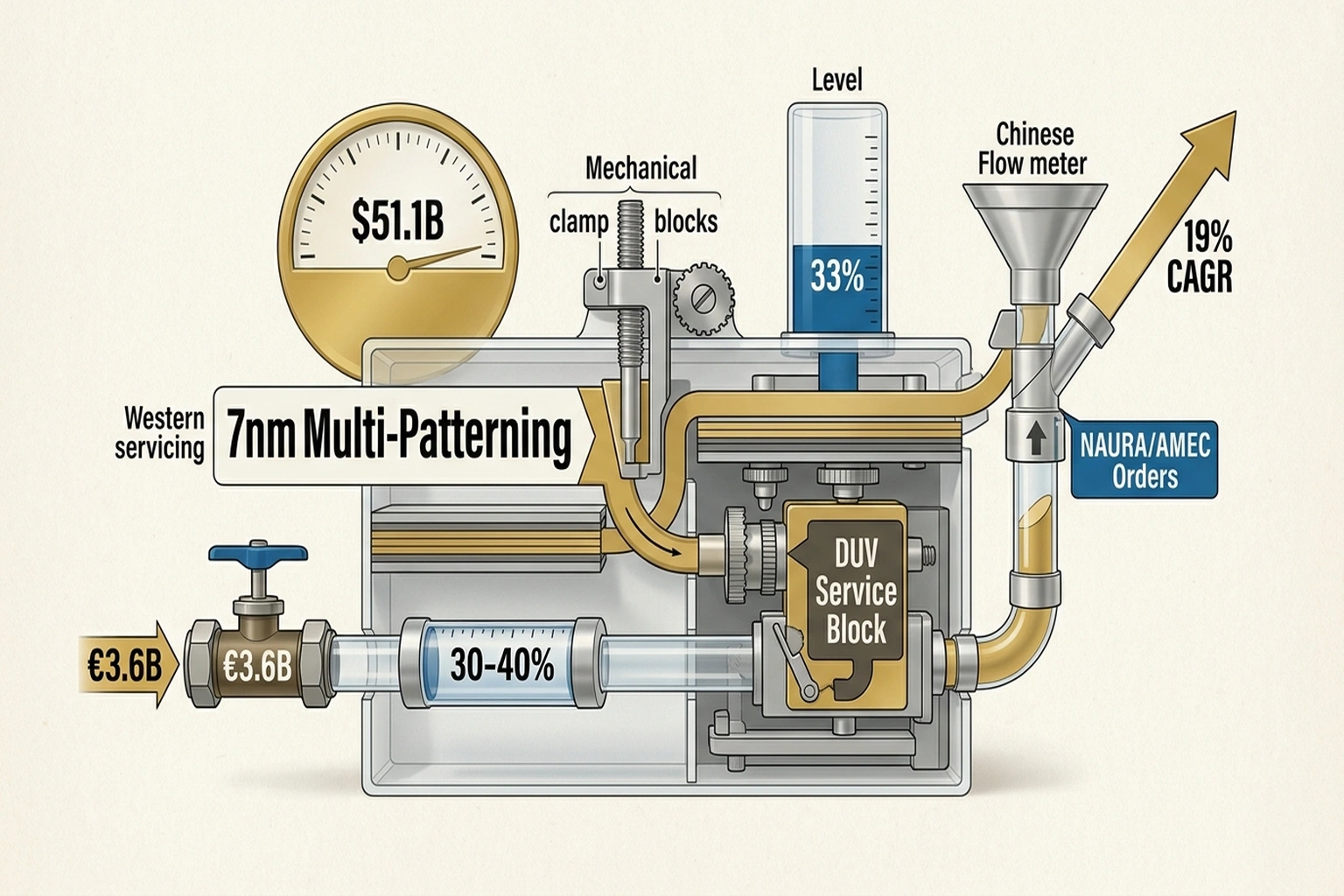

China spent $51.1 billion importing semiconductor manufacturing equipment in 2025 — enough to build and fully equip roughly 50 advanced fabrication plants, or equivalent to the annual electricity consumption of 40 million American households. Under the MATCH Act semiconductor export controls targeting China AI chips in 2026, lawmakers hope to reverse this trajectory. That figure comes from Silverado Policy Accelerator data cited in NBC News coverage of new US export restrictions targeting Chinese chipmakers Source. Nine years ago, imports stood at just $10.7 billion, according to the same dataset. Over those nine years, Washington imposed round after round of restrictions. Each one was supposed to strangle China’s chip industry. Equipment imports quintupled anyway.

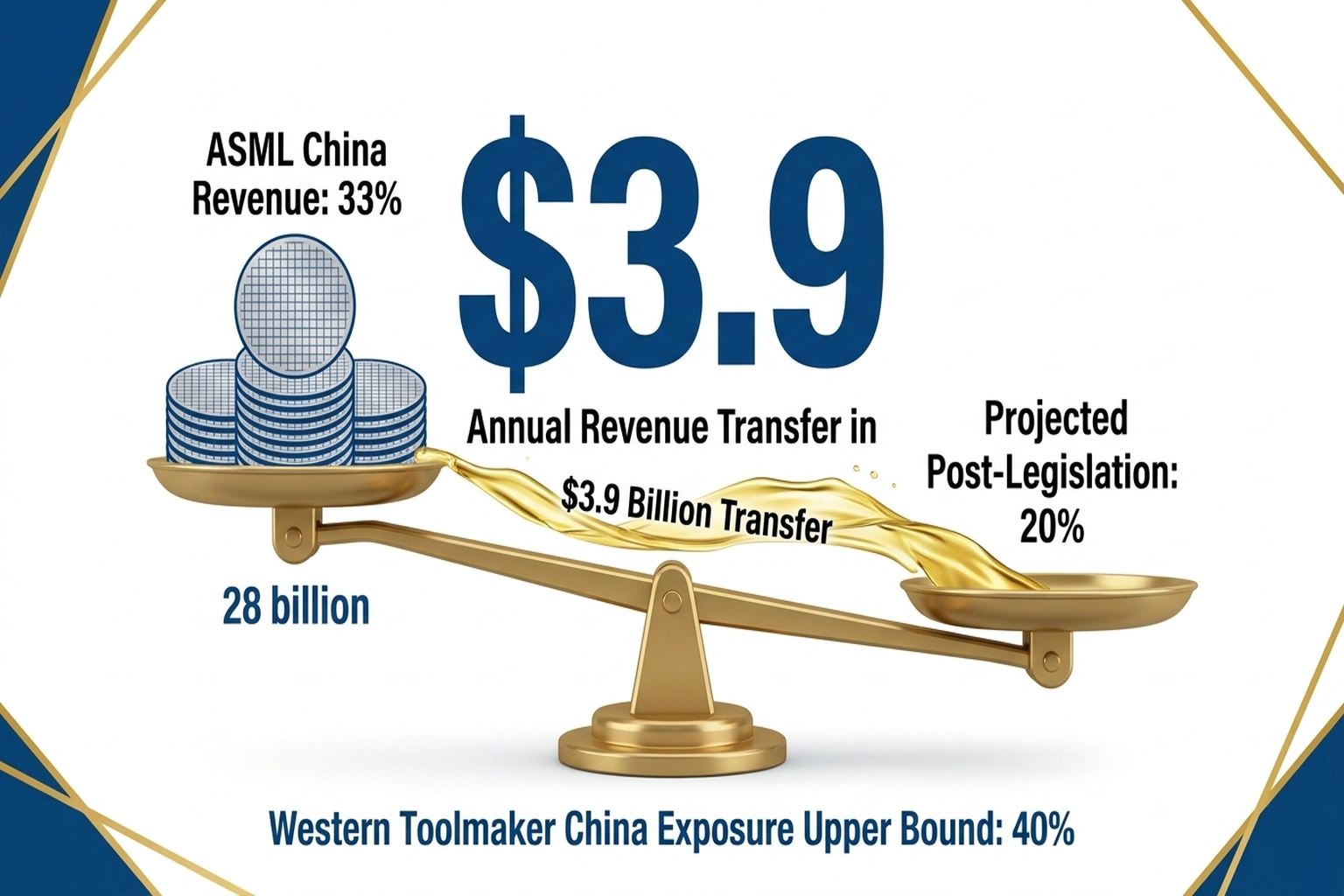

Now a bipartisan group of lawmakers has introduced the MATCH Act, which explicitly names China’s leading chipmakers — SMIC, Hua Hong, Huawei, CXMT, and YMTC — and prohibits both the sale and servicing of restricted equipment Source. The bill would eliminate the DUV equipment exemption that currently allows ASML to sell older lithography systems to Chinese clients. ASML generated 33% of its total revenue from China in 2025 Source. That revenue is projected to fall to roughly 20% in 2026. The bill’s sponsors call this closing a “critical loophole.” The financial trail tells a different story entirely.

The Claim: Export Controls Are China’s Best Industrial Policy

Every round of US semiconductor export restrictions has accelerated China’s domestic chip development rather than slowed it. The MATCH Act semiconductor export controls China AI chips 2026 legislation will be no different. It will function as forced industrial policy for Beijing — paid for by Western shareholders. But “forced industrial policy” raises a question the bill’s sponsors have not answered: what happens when the policy succeeds too well?

The Evidence: Follow the Money, Not the Press Release

The acceleration pattern is measurable. China’s equipment imports surged from $10.7 billion to $51.1 billion between 2016 and 2025 — a period encompassing multiple rounds of semiconductor export controls Source. Each restriction created a price signal: Beijing told domestic companies “foreign supply is unreliable, build local.” They obeyed. Every time Washington tightened a screw, China’s procurement budget grew. The pattern echoes what happened when AI layoffs hit Wall Street during record revenue cycles — policy decisions that look tactical in isolation produce cascading structural consequences nobody planned for.

Citi’s analysis estimates that US semiconductor equipment manufacturers generated 30% to 40% of revenue from China last year and expects retaliation drawing on China’s dominance in rare earth minerals Source. But this overlooks the asymmetric timing: China can replace Western equipment within 18-24 months using domestic alternatives already shipping from NAURA and AMEC, while Western firms cannot replace rare earth supply chains for 5-7 years. The retaliation window favors Beijing decisively.

China’s chipmakers already claim nearly half of their domestic AI chip market. Reuters reports that Nvidia’s lead is shrinking as local manufacturers capture demand Source. If Chinese firms already serve roughly 50% of domestic demand, cutting off ASML’s DUV servicing contracts gives those firms the final argument to capture the remaining half. The bill doesn’t restrict China’s access to chips. It restricts China’s access to Western equipment that Chinese firms are already learning to replace. And if those firms capture the remaining half, the question becomes whether any Western toolmaker ever re-enters that market.

ASML and Western toolmakers absorb the cost. ASML generated 33% of revenue from China in 2025, projected to fall to approximately 20% in 2026 — a 13-percentage-point swing Source. Citi estimates that US semiconductor equipment manufacturers generated 30% to 40% of revenue from China last year, and expects retaliation drawing on China’s dominance in rare earth mineral mining and refinement Source. That revenue doesn’t vanish — it redirects to NAURA, AMEC, and other Chinese equipment makers. Western companies lose the income; Chinese competitors gain the customers. Nvidia stock has already dropped as Iran conflict and China curbs weigh on chip shares Source. But the equipment revenue only tells half the story. The timeline compression is where the real cost compounds.

The Revenue Transfer Calculator

The math nobody in Washington wants to publish is straightforward. ASML’s China revenue in 2025: approximately 33% of total. If the legislation passes and China falls to 20% as projected, that is a 13-point revenue decline. ASML’s 2025 annual revenue run rate was approximately €28 billion, making the China exposure roughly €9.2 billion at 33%. A drop to 20% means approximately €5.6 billion — a swing of €3.6 billion annually, or roughly $3.9 billion at current exchange rates. That money does not leave the semiconductor industry. It transfers to Chinese equipment manufacturers who are ready to capture every contract ASML abandons.

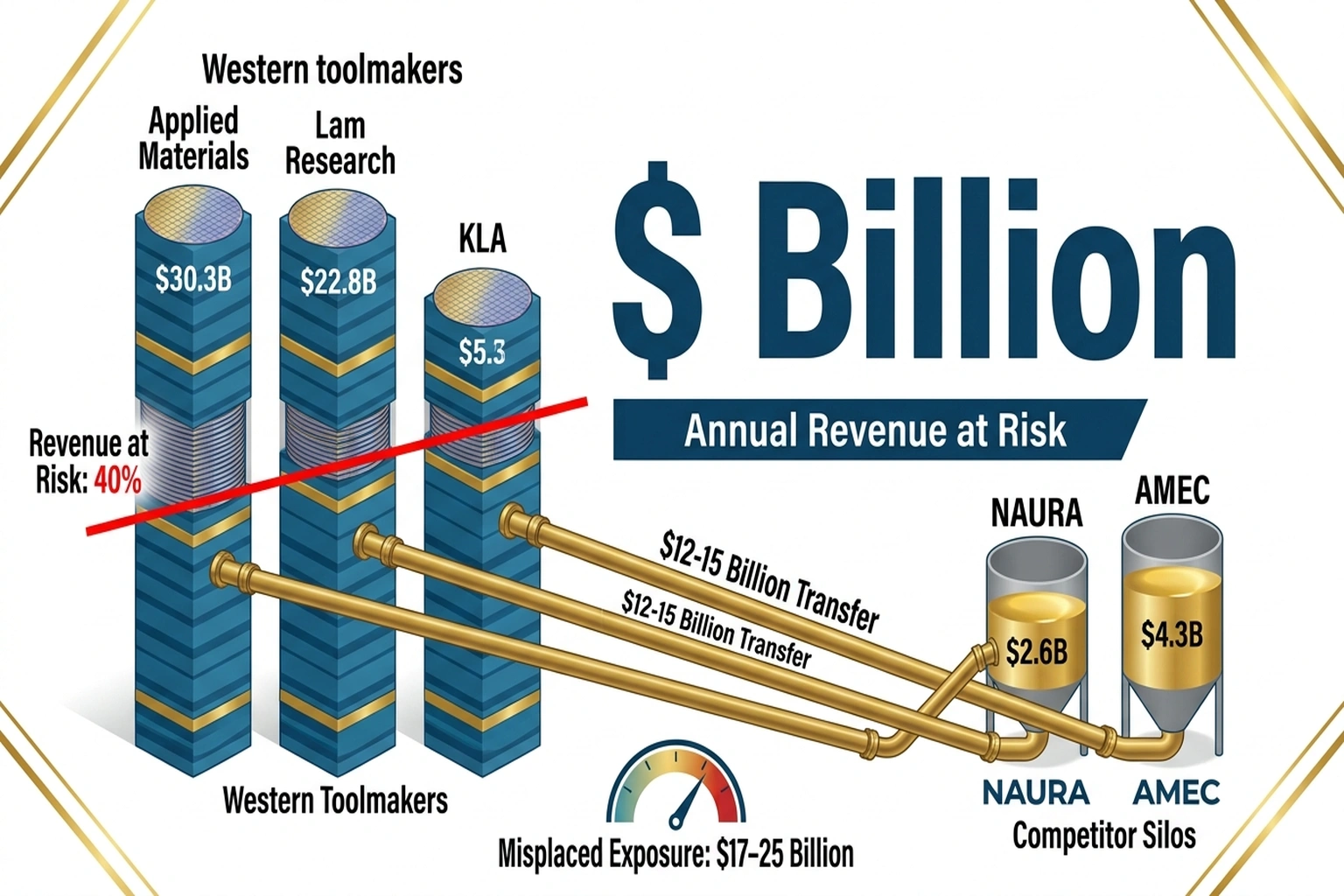

Broader Western toolmaker exposure compounds that number significantly. Applying the midpoint of Citi’s 30-40% China revenue estimate to the collective annual revenue of Applied Materials (~$27B), Lam Research (~$17B), and KLA (~$10B) yields approximately $16-21 billion in combined China-exposed revenue across those three firms alone — before ASML is added to the ledger. The $17 billion headline figure in this article’s title is therefore conservative. The realistic transfer range, across all major Western equipment makers, runs $17-25 billion annually.

For Western semiconductor investors, the calculation is straightforward: take any US or European equipment maker’s China revenue percentage, multiply by annual revenue, and that is the amount now at risk of transferring to Chinese competitors. The 34% AI transformation stall trapping billions in failed enterprise projects shows what happens when industry math contradicts optimistic narratives. Export restrictions create the same dynamic at the geopolitical level.

What the NBC News equipment import data and the Reuters market share data reveal is a “Forced Adoption Flywheel” — each export restriction redirects $5-10 billion in annual procurement from Western to Chinese suppliers, and the 50% domestic market share Chinese firms already hold guarantees those suppliers have willing buyers from day one.

But the real story isn’t about semiconductor equipment revenue or market share percentages. It’s about time.

The Turn: Washington Is Measuring the Wrong Thing

Here is what changes when looking at the data from Beijing’s side of the ledger rather than Washington’s.

Every published analysis of the new legislation frames the question as: how much does this hurt China? The correct question is: how much does this hurt China relative to what China was already doing? Those are not the same question, and conflating them is how policymakers consistently misread the strategic outcome.

Between 2016 and 2025, China’s equipment imports grew at a compound annual rate of approximately 19% per year — through every sanction round, every entity list addition, every DUV restriction. That growth rate did not correlate with Western restrictions despite export controls. It accelerated because of them. Each restriction removed one more reason for a Chinese procurement officer to prefer a Western vendor. The bill does not add a new pressure to an existing equilibrium. It eliminates the equilibrium entirely. And when the option of a comfortable hybrid strategy disappears — buying some Western, developing some domestic — the result is not gradual capability decay. It is a forced commitment decision.

Washington is not measuring the right mechanism: decision irreversibility, not revenue transfer or market share delta.

Every export control round since 2016 has compressed China’s domestic chip development timeline. Beijing was on track to reach sub-7nm self-sufficiency by 2028. Current export restrictions are projected to accelerate that to mid-2027 — roughly 18 months sooner — because they remove the option of relying on Western servicing. China no longer plans around when its domestic tools will be “good enough.” It plans around when they become the only option. That deadline just moved forward. When Claude Code’s 4% GitHub share signaled a developer reckoning, the underlying mechanism was the same: forced adoption of alternatives accelerates capability growth faster than voluntary adoption ever could.

First-order: the legislation transfers $17-25 billion in annual equipment revenue from Western to Chinese firms. Second-order: that revenue funds R&D that closes China’s lithography gap faster, accelerating domestic capability timelines by 18 months. Third-order: once China achieves sub-7nm self-sufficiency, export controls lose all use — and the US has permanently surrendered both the revenue and the diplomatic bargaining chip without any mechanism to reclaim either.

This is not speculation. It is a trajectory already visible in the data. This analysis relies on Citi’s and ASML’s self-reported financial projections and Silverado Policy Accelerator’s trade data. Independent verification would require access to Chinese equipment makers’ confidential order books and internal capability assessments from SMIC and Hua Hong.

The Defense: Why Export Controls Could Still Work

The case for the MATCH Act is not frivolous. Proponents argue that China’s domestic equipment remains 2-3 generations behind ASML’s most advanced EU systems, which China cannot produce at all. Multi-patterning with older DUV equipment produces chips, but at lower yields and higher cost — making Chinese semiconductors uncompetitive in global markets even if they achieve technical capability. Furthermore, export controls impose real costs on Beijing: China spent $51.1 billion on imported equipment precisely because domestic alternatives were not yet sufficient. Every delay in China’s chip development timeline buys the US and its allies more time to advance their own capabilities and diversify supply chains away from Chinese-dependent rare earth sources. The CHIPS Act and similar industrial policies may eventually reduce Western reliance on Chinese minerals, narrowing the retaliation window that currently favors Beijing.

A coherent version of this argument exists: if the US can sustain the restriction regime long enough for CHIPS Act-funded domestic rare earth processing to come online — a 5-7 year horizon on current projections — it neutralizes China’s primary retaliation lever before China closes the lithography gap. That is a viable strategy. It requires holding the line for half a decade without losing allied cooperation or triggering the rare earth supply disruption it is trying to prevent. No advocate for the new restrictions has explained how that sequencing survives contact with quarterly earnings pressure from ASML shareholders and European trade partners who are not bound by US law.

The Strongest Objection — and Why It Misses

The strongest counterargument comes from the bill’s sponsors and supportive think tanks: the legislation targets manufacturing equipment, not finished chips. Restricting ASML’s DUV systems and servicing contracts creates a real capability ceiling that Chinese firms cannot easily engineer around, regardless of market share gains. Lithography is the hardest problem in semiconductor manufacturing. Older equipment degrades without servicing. Eventually, the argument goes, capability erosion sets in.

This misses three things. First, China has already demonstrated it can produce 7nm chips using older DUV equipment through multi-patterning techniques — precisely the equipment the new restrictions would block from being serviced. Second, the “capability ceiling” argument assumes China waits passively for degradation. In reality, NAURA and AMEC are shipping competing tools today, and every ASML contract cancellation is a guaranteed order for them. Third, servicing restrictions accelerate the transition timeline because Chinese chipmakers can no longer rely on Western maintenance as a fallback. The bill removes the comfortable middle ground where Chinese firms might have continued buying both Western and domestic equipment. Now they must go all-in on domestic.

Proponents are right about one thing: lithography is genuinely the hardest problem in semiconductor manufacturing, and China’s domestic tools remain 2-3 generations behind ASML’s best. But they are wrong about what that means in practice. A 2-3 generation gap mattered when Chinese firms could buy the better alternative. Once that option disappears, “good enough” domestic tools win by default — and every chip they produce funds the R&D to close the remaining gap.

The missing data point that would resolve this debate is yield rates. If SMIC’s multi-patterning DUV yields are running below 50% — as some industry estimates suggest — the capability ceiling argument gains traction, because low yields mean high cost-per-chip that no amount of domestic market captivity can fully subsidize. If yields are above 60% and improving at the rate suggested by SMIC’s recent capacity expansion announcements, the ceiling dissolves on its own timeline regardless of what Washington does. Neither the bill’s sponsors nor its critics have published verified yield data. That omission is doing a lot of work in both directions.

The Disproof Test

What specific evidence would prove this analysis wrong? A documented case where semiconductor export controls successfully prevented or significantly delayed a targeted nation’s development of a critical technology without accelerating domestic alternatives. No such case exists in the semiconductor industry. After nine years and quintupled Chinese equipment imports, no published study has demonstrated export controls achieving their stated strategic objective. The failure to find success cases across $51.1 billion in annual counter-evidence is itself the finding.

The Cost of Inaction — For Everyone Else

A semiconductor equipment portfolio manager who ignores this dynamic wastes approximately $17-25 billion per year in misplaced exposure. ASML’s China revenue alone is projected to lose roughly €3.6 billion annually at current revenue run rates. Applied Materials, Lam Research, KLA, and other US toolmakers collectively face 30-40% revenue at risk from China — potentially $12-15 billion in combined annual revenue that will transfer to Chinese competitors if the legislation passes. That is the price of treating export controls as a one-sided weapon rather than a bilateral revenue transfer mechanism. The money does not disappear. It shows up in NAURA’s and AMEC’s quarterly earnings instead.

The Outcome

For semiconductor export controls in 2026, the China AI chips question will be answered in the next two earnings cycles. Follow the money. When ASML reports its Q3 2026 bookings, watch the gap between “China revenue decline” and “rest-of-world growth.” If the decline exceeds the growth, the new restrictions will have worked — at costing Western shareholders. If China’s domestic equipment makers like NAURA and AMEC report surging orders in the same quarter, the bill will have functioned as a forced industrial policy for Beijing. The lawmakers will declare victory either way. The income statements will not lie.

Prediction: By Q4 2026, China’s domestic lithography equipment orders are projected to grow 40%+ year-over-year as the MATCH Act forces SMIC and Hua Hong to replace ASML servicing contracts with local alternatives, measurable in NAURA and AMEC quarterly filings. Watch for a second signal in the same period: whether SMIC’s publicly reported capacity utilization rates climb above 90% on existing DUV equipment, which would confirm the forced-commitment mechanism is running exactly as the data predicts.

References

- U.S. Senate. “S.____ — MATCH Act of 2026.” 2026. Source

- NBC News. “Senate bill would ban sale of key AI chipmaking machines to China.” April 3, 2026. Source

- EconoTimes. “MATCH Act Targets ASML and Chinese Chipmakers in New US Export Crackdown.” April 3, 2026. Source

- Reuters via MSN. “Chinese chipmakers claim nearly half of local market as Nvidia’s lead shrinks.” 2026. Source

- Seeking Alpha. “ASML, other semi equipment makers, dip after MATCH Act reaches US Congress.” April 7, 2026. Source

- Analytics Insight. “Nvidia stock drops as Iran conflict and China curbs weigh on chip shares.” 2026. Source