12 min read · 3,118 words

According to World Nuclear News , “Constellation to, global data centre electricity consumption reached approximately 415 terawatt-hours (TWh) in 2024, representing about 1.5% of global electricity use, according to the International Energy Agency. That figure is growing at 12% annually, driven primarily by AI workloads. By 2030, data centre electricity consumption is projected to reach around 945 TWh in the IEA’s base-case scenario – more than doubling in 6 years. The North American grid, designed for gradual demand growth over decades, cannot expand transmission capacity fast enough. Connection queues for new data centre power contracts have stretched to seven years in some regions. Data centre demand in the PJM electricity market, stretching from Illinois to North Carolina, accounted for an estimated $9.3 billion price increase in the 2025-26 capacity market alone. It is in this climate that Microsoft signed a 20-year agreement to restart Three Mile Island’s dormant reactor.

The symbolism is impossible to miss. The site of America’s worst nuclear accident becomes a response to the most urgent AI constraint yet, and the company underwriting the deal isn’t a utility, but a technology giant whose data centers now consume more electricity than some countries. In rapid succession, Google followed with a fleet agreement for small modular reactors. Amazon led a $500 million funding round for X-energy. The United States government, recognizing the gravity of the situation, approved the country’s first fully integrated nuclear-powered AI campus at Idaho National Laboratory on February 13, 2026. This isn’t green energy idealism. The hyperscaler AI power bottleneck has become an existential constraint on the expansion of artificial intelligence – and the companies building the future of computing have concluded that buying nuclear reactors is faster than waiting for the grid to catch up. (The Guardian , “Google to buy nucl)

The Energy Crisis Behind Every AI Query

Economics driving Big Tech’s nuclear pivot stem from a fundamental mismatch between AI’s power appetite and the reality of infrastructure. Training a single frontier model now requires gigawatt-hours of electricity – enough to power thousands of U.S. homes for a year, or to keep a small city’s lights on for several weeks. Inference at scale – the daily barrage of ChatGPT queries, image generations, and code completions – demands continuous baseload power that renewable sources cannot guarantee without massive battery storage that doesn’t yet exist at the required scale. Data center power demand in the United States has surged, with AI workloads accounting for the majority of that growth. The North American electric grid, designed for gradual demand growth over decades, cannot expand transmission capacity fast enough. In Loudoun County, Virginia, for example, a major hyperscale data center operator has awaited grid connection approval since 2019 – a delay now stretching beyond five years, with local utility officials unable to guarantee an in-service date before 2027. This is not an isolated case: connection queues for new data center power contracts have stretched to seven years in some regions. For companies whose market valuations depend on AI infrastructure scaling, that timeline represents an unacceptable competitive risk. The constraint isn’t merely capacity – it’s reliability. AI training runs cannot tolerate power interruptions. A single outage during a multi-million-dollar model training session means restarting from checkpoints, wasting GPU hours that cost tens of thousands of dollars per hour. Reliability: Solar and wind, despite their cost advantages, introduce intermittency that hyperscalers cannot absorb at current battery technology levels. Unplanned outages and fluctuating supply are simply unacceptable for AI workloads, which require continuous, unbroken power to avoid massive financial losses. Emissions: At the same time, the industry cannot simply revert to fossil fuels for energy security. Carbon regulations and climate commitments make low-emission electricity a non-negotiable requirement. Nuclear power offers what no other source can: carbon-free electricity available 24 hours a day, 365 days a year, with the grid independence that comes from owning the generation asset.

Microsoft’s Three Mile Island Play: The Deal Structure

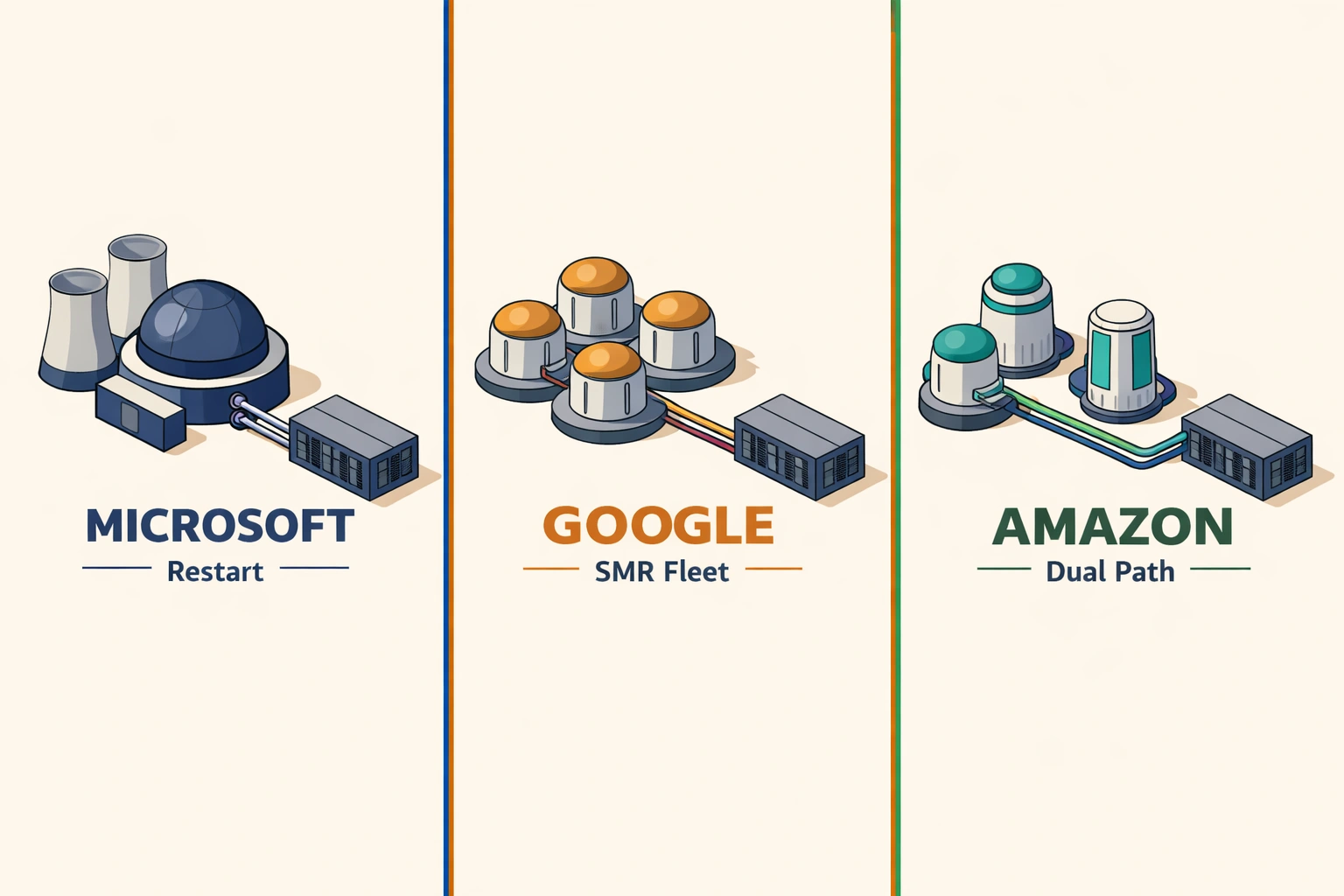

Microsoft’s agreement with Constellation Energy to restart Unit 1 of the Three Mile Island facility, now renamed the Crane Clean Energy Center, represents the most concrete nuclear-to-AI transaction to date. The 20-year power purchase agreement guarantees Microsoft access to 835 megawatts of carbon-free baseload power beginning in 2027, pending regulatory approval for the reactor restart. Constellation Energy stated in its September 2024 announcement that significant investments will be made to restore the facility, including the turbine, generator, main power transformer, and cooling and control systems. The plant aims to be online by 2028. The financial terms remain undisclosed, but the structure signals how hyperscalers view energy security. Rather than purchasing power from existing nuclear plants, Microsoft is effectively funding the restart of a decommissioned facility. Constellation Energy, the largest nuclear operator in the United States, gains a guaranteed revenue stream that makes the economics of restarting a 45-year-old reactor viable. Microsoft gains exclusive access to generation capacity that cannot be diverted to competitors. This isn’t Microsoft’s first nuclear foray. The company has previously announced partnerships to explore fusion energy and has invested in next-generation reactor designs. The Three Mile Island deal represents a different strategy: securing proven technology at scale within a defined timeline. The reactor exists. The regulatory framework exists. The primary obstacles are operational rather than technological – making this a deployment play rather than a research bet. Constellation’s stock performance reflects market recognition of this shift. The company’s projected 2026 earnings growth exceeds 20%, driven largely by premium pricing from AI-focused power purchase agreements. The nuclear operator has effectively positioned itself as an infrastructure partner for the AI economy rather than a traditional utility.

Google and Amazon: Betting on Small Modular Reactors

According to International Energy Agency , “Energy d, side-by-side comparison of Google’s SMR fleet strategy versus Amazon’s diversified nuclear investment portfolio. Google’s approach diverges from Microsoft’s restart strategy. The company secured a fleet agreement with Kairos Power to deploy Small Modular Reactors (SMRs) – a newer technology that promises faster deployment, lower capital costs, and siting flexibility that traditional reactors cannot match. The October 2024 agreement targets adding 500 MW of nuclear power starting at the end of the decade, with the first reactor potentially online by 2030 and additional reactors through 2035. Amazon split its nuclear bets across multiple technologies. The company led a $500 million funding round for X-energy, an SMR developer pursuing a different reactor design than Kairos, as announced in October 2024. Amazon Web Services has simultaneously explored partnerships with existing nuclear facilities to colocate data centers adjacent to generation assets – a strategy already employed at the Cumulus facility in Pennsylvania, which Amazon acquired in 2024. The SMR thesis rests on manufacturing economics that have yet to be proven at a commercial scale. Traditional nuclear plants require custom engineering for each installation, driving costs and timelines that have killed projects for decades. SMRs promise factory-built modules that can be transported to sites and assembled with standardized processes. The ambition echoes the transformation of the aircraft industry in the mid-20th century, when moving from bespoke aircraft to standardized, mass-produced airliners slashed costs and enabled rapid global expansion. If the nuclear manufacturing model succeeds, SMRs could allow hyperscalers to deploy dedicated nuclear capacity at multiple locations without the decade-long timelines of traditional reactor construction. Yet, like early attempts at industrial aircraft production, this leap remains more promise than reality until proven at scale. The risk is that SMR economics remain theoretical. NuScale Power, the most advanced SMR developer in the United States, only recently reached Final Investment Decision for a 462-megawatt project in Romania – its first commercial deployment after years of regulatory delays and cost revisions. The technology is promising but unproven at the scale hyperscalers require.

Google and Amazon: Betting on Small Modular Reactors

Google and Amazon: Betting on Small Modular Reactors

The Idaho National Laboratory Blueprint: Islanded from the Grid

On February 13, 2026, the most ambitious nuclear-AI project advanced when a consortium led by Swiss-American firm Deep Atomic submitted final planning documents to the Department of Energy for a fully integrated nuclear-powered data center campus at Idaho National Laboratory. The project’s defining characteristic is grid independence. Unlike nuclear-adjacent data centers that draw from the same grid as other consumers, the Idaho facility appears designed to be entirely “islanded” – operating on dedicated nuclear generation without connection to public utility infrastructure. Deep Atomic’s MK60 Small Modular Reactor would provide 60 megawatts of electrical power and, critically, 60 megawatts of integrated cooling capacity by recycling reactor heat to chill AI server racks. The cooling integration represents a technical innovation that could define future nuclear-AI designs. Data centers typically spend 30-40% of their power budget on cooling systems. By capturing waste heat from the reactor for cooling processes, the Idaho project claims dramatic efficiency improvements that could reshape the economics of nuclear-powered computing. The consortium includes Paragon Energy Solutions for nuclear components, Future-tech for data center engineering, and Clayco for integrated design and construction. The Department of Energy has leased 44,000 acres at Idaho National Laboratory for the initiative, part of a 2025 executive push to treat AI infrastructure as a national security priority. If successful, the model could be replicated at Oak Ridge, Tennessee; Savannah River, South Carolina; and the Paducah site, Kentucky. The timeline is aggressive. The data center component could launch within 24 to 36 months using existing on-site geothermal and solar power while the nuclear reactor completes certification. Full nuclear operation is targeted for the 2030s. The Nuclear Regulatory Commission has never approved a commercial SMR on this timeline – a track record that should give pause regarding whether this ambitious schedule can be met.

The Policy Foundation: ADVANCE Act and COP30 Commitments

According to The Register , “US is moving ahead with, nuclear resurgence isn’t happening in a regulatory vacuum. The ADVANCE Act, signed into law in mid-2024, streamlined Nuclear Regulatory Commission (NRC) licensing processes and reduced fees for advanced reactor designs. Prior to the Act, NRC licensing fees for new reactors could exceed $30 million and take 7 to 10 years to obtain approval. After the Act’s reforms, typical licensing costs have dropped to around $10 million, with review timelines of 3 to 5 years. By February 2026, the NRC had fulfilled nearly all its mandates to accelerate deployment. Industry participants describe this regulatory transformation as the most significant in decades – one that translates directly to faster, less expensive nuclear projects and a dramatically changed economic equation for AI-focused infrastructure. International policy has aligned with U.S. action. The COP30 summit in late 2025 saw more than 30 nations pledge to triple their nuclear capacity by 2050, providing long-term policy certainty that had been absent since the post-Fukushima era. The commitment signals to capital markets that nuclear investment carries government backing across electoral cycles – a critical factor for infrastructure with 60-year operational lifespans. The policy alignment reflects a strategic calculation: AI leadership requires energy independence. The race to dominate artificial intelligence is inseparable from the race to control the energy sources that power it. Nations that cannot guarantee carbon-free baseload power for AI infrastructure will cede competitive advantage to those that can. The pressure for energy security is no longer abstract national policy but a boardroom imperative, driving hyperscalers to treat infrastructure as a domain of corporate strategy as much as government interest. As policy and C-suite priorities converge, the distinction between national security and corporate survival blurs.

The Three Horizons Framework for Nuclear-AI Integration

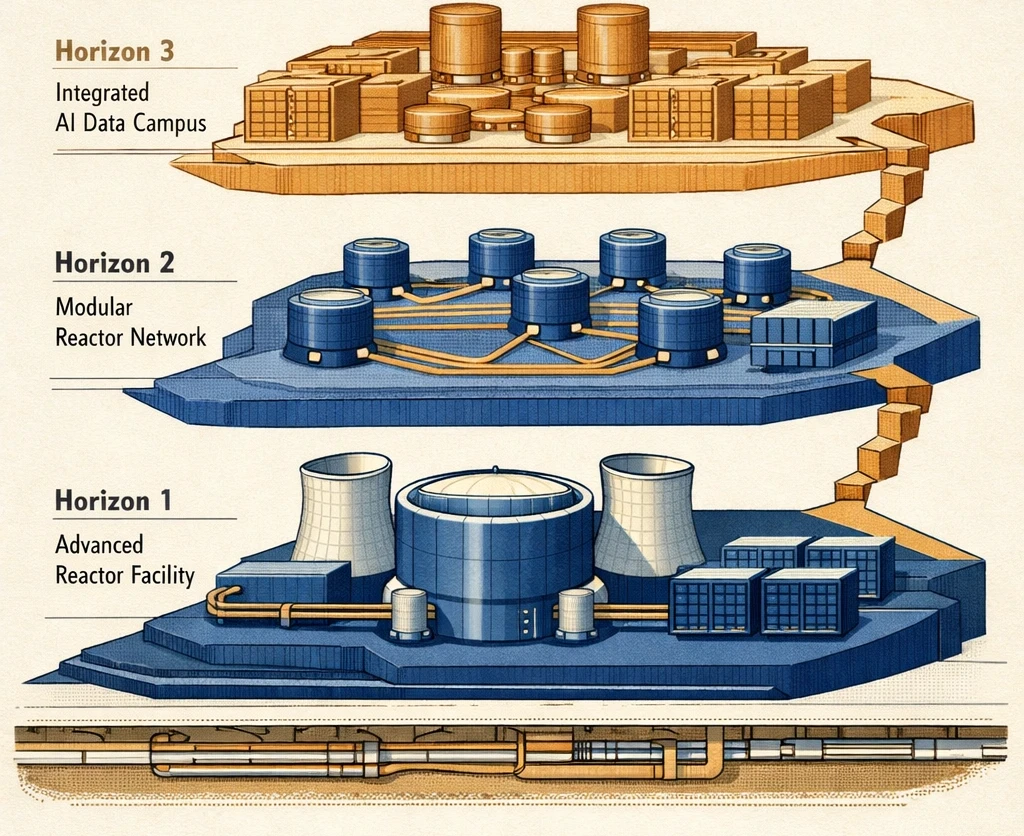

Three-phase timeline showing nuclear-AI integration horizons from 2026 reactor restarts through 2035 advanced deployment The current wave of nuclear investment can be understood through a framework (original synthesis for this analysis) that clarifies timelines and risk profiles: Horizon One (2026-2029): Reactor Restarts and Co-location – Microsoft’s Three Mile Island deal exemplifies this phase – using existing nuclear infrastructure to secure baseload power within predictable timelines. These projects face regulatory hurdles but no technological uncertainty. Horizon Two (2028-2034): First SMR Deployments – Google’s Kairos partnership and Amazon’s X-energy investment target this window. Success depends on SMR manufacturers delivering factory-built reactors at projected costs and timelines – a technological risk that restart projects avoid, but that offers superior economics if achieved. Horizon Three (2030+): Integrated Nuclear-AI Campuses – The Idaho National Laboratory project represents the furthest horizon: purpose-built facilities where the reactor and data center are designed as integrated systems. These projects offer maximum efficiency but require the longest lead times. The fuel supply chain presents another constraint. The 2024 ban on Russian enriched uranium created an immediate supply gap. Uranium spot prices hover near $100 per pound, with Western producers like Cameco capturing significant value. High-Assay Low-Enriched Uranium (HALEU), required for SMRs, has limited Western production capacity – a bottleneck that could constrain deployments even if reactor technology matures on schedule. If HALEU output fails to scale in time, the consequences ripple quickly. Some hyperscaler contracts for SMR power may trigger fallback provisions to conventional gas-fired generation, undermining decarbonization targets and exposing operators to fossil fuel price volatility. Others might simply stall, freezing capital in incomplete projects and leaving critical AI infrastructure plans delayed by years. In either scenario, supply chain fragility elevates uranium sourcing and enrichment capacity to a board-level strategic risk, forcing technology leaders to consider vertical integration or direct investment in Western nuclear fuel production as insurance against future shortages.

The Three Horizons Framework for Nuclear-AI Integration

The Three Horizons Framework for Nuclear-AI Integration

Market Implications and Competitive Dynamics

A fundamental re-rating of utility and uranium stocks has been triggered by the nuclear pivot. Constellation Energy and Vistra Corporation have emerged as the primary beneficiaries of AI-driven power demand. Vistra’s procurement partnership with Meta Platforms, announced in early 2026, demonstrates that nuclear operators can extract premium pricing from hyperscalers willing to pay for reliability guarantees. This analysis suggests traditional independent power producers relying on intermittent renewables face a more challenging competitive position. As markets shift focus to “firm” power – generation available on demand rather than weather-dependent – companies without nuclear or dispatchable capacity may see their assets repriced as lower-value. The consolidation wave has already begun. SMR startups that cannot secure hyperscaler partnerships face capital constraints as investors concentrate bets on companies with demonstrated technology and signed power purchase agreements. The evidence suggests the next five years will likely see a shakeout that leaves a handful of SMR developers with the scale to compete for utility and hyperscaler contracts.

The Geopolitical Dimension

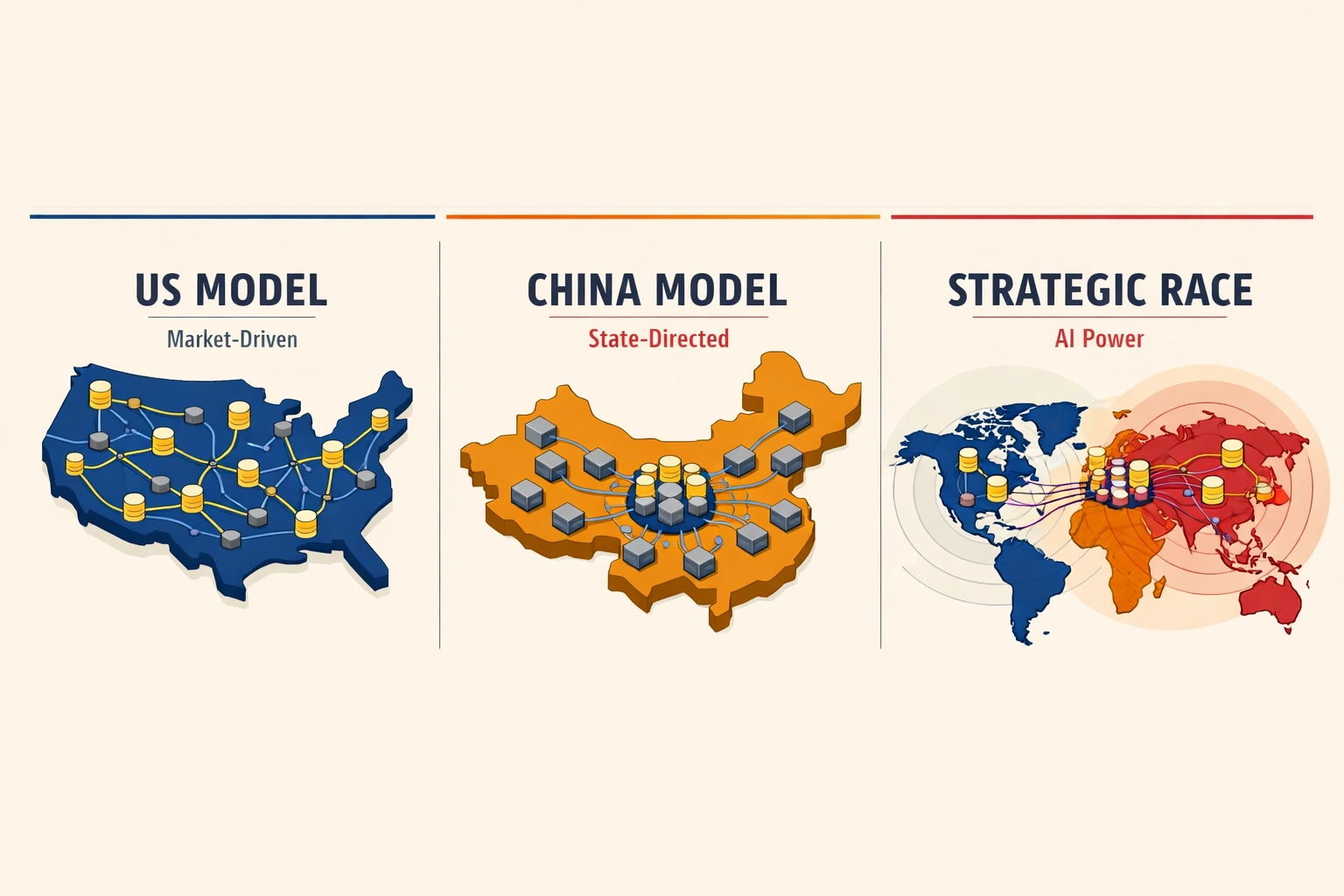

Global map contrasting the US private-capital nuclear model against China’s state-directed expansion approach.China currently builds more reactors than any other nation, pursuing a state-directed nuclear expansion that could secure energy independence for its AI infrastructure. The U.S. response, using private capital from hyperscalers with government support through regulatory streamlining and federal land access, represents a different model but the same strategic objective. The centralization-versus-market-driven-collaboration question remains open: which governance style will deliver new reactors faster, and how will that speed affect the global balance of AI infrastructure? The decoupling from Russian uranium supplies has accelerated Western investment in domestic fuel cycles. This supply chain independence is treated as a national security imperative, not merely an economic optimization. The same logic that drove semiconductor reshoring now applies to nuclear fuel: dependence on adversarial sources for critical infrastructure creates unacceptable vulnerability.

The Geopolitical Dimension

The Geopolitical Dimension

Key Milestones Ahead

Three indicators will determine whether the nuclear resurgence delivers on its promise: The Three Mile Island restart timeline. If Constellation brings the Crane Clean Energy Center online ahead of its 2028 target, it validates the restart model as a rapid path to additional capacity. Delays or cost overruns would signal that even proven technology faces execution risk. SMR regulatory approvals. The Nuclear Regulatory Commission has never approved a commercial SMR for operation. The first approval will establish precedent for subsequent projects and determine whether the promised advantages of the timeline materialize. Uranium production scaling. Western producers must increase output significantly to meet demand from new reactor projects. Supply shortages could cap deployment rates regardless of regulatory progress. The hyperscaler AI power bottleneck has forced a strategic recalibration across the technology industry. Companies that spent the last decade optimizing for carbon neutrality through renewable energy purchases have concluded that nuclear power – the same technology environmental activists opposed for decades – now represents the only viable path to both climate goals and AI competitiveness. The reactor purchases aren’t ideological. They’re survival math.

The strongest counterargument is that the nuclear pivot represents a dangerous distraction from scaling grid storage and long-duration battery technology, which critics argue is already on a steeper cost-reduction curve than nuclear has ever achieved. Proponents of this view contend that hyperscaler capital commitments to nuclear are effectively locking in a high-cost, high-risk baseload solution at precisely the moment when accelerated investment in grid-scale storage could deliver the same reliability outcomes without the decade-long lead times or waste disposal liabilities. On this reading, Big Tech is not solving the AI energy crisis so much as perpetuating it by channeling billions away from the faster-maturing technologies that could resolve it within the same 2030 window.

What to Read Next

- The 30-Minute Trap: Alibaba’s AI Agent Meets Unprepared Buyers

- The 34% Problem: AI Transformation Stalls, Traps Billions

- The 80% AI Project Failure Rate Costs Firms $7.2M Each

References

- World Nuclear News , “Constellation to restart Three Mile Island unit, powering Microsoft” , Details Microsoft’s 20-year power purchase agreement with Constellation Energy for the Three Mile Island restart, renamed Crane Clean Energy Center, targeting 2028 operation.

- International Energy Agency , “Energy demand from AI – Energy and AI” , Provides data centre electricity consumption projections showing 415 TWh in 2024, growing to approximately 945 TWh by 2030, with 12% annual growth driven by AI workloads.

- The Register , “US is moving ahead with colocated nukes and datacenters” , Provides technical details on Deep Atomic’s MK60 SMR, consortium partners including Clayco and Paragon Energy Solutions, and analyst perspectives on SMR timelines.

- The Guardian , “Google to buy nuclear power for AI datacentres in ‘world first’ deal” , Reports on Google’s agreement with Kairos Power to purchase nuclear energy from multiple SMRs, targeting the first commercial reactor by 2030 and a 500 MW fleet by 2035 to support AI data centre energy needs.

- X-energy , “Amazon Invests in X-energy to Support Advanced Small Modular Nuclear Reactors” , Announces Amazon’s approximately $500 million Series C-1 financing round in X-energy, supporting deployment of up to 5 GW of SMR capacity by 2039 for data centre power needs.